In the Absence of Uncertainty, There Is No Reward

In investing, uncertainty is often cast as the villain. It unsettles markets, shakes confidence, and tempts us to retreat to the safety of cash. But this view misses a fundamental truth: uncertainty is not the enemy—it is the very condition that makes reward possible.

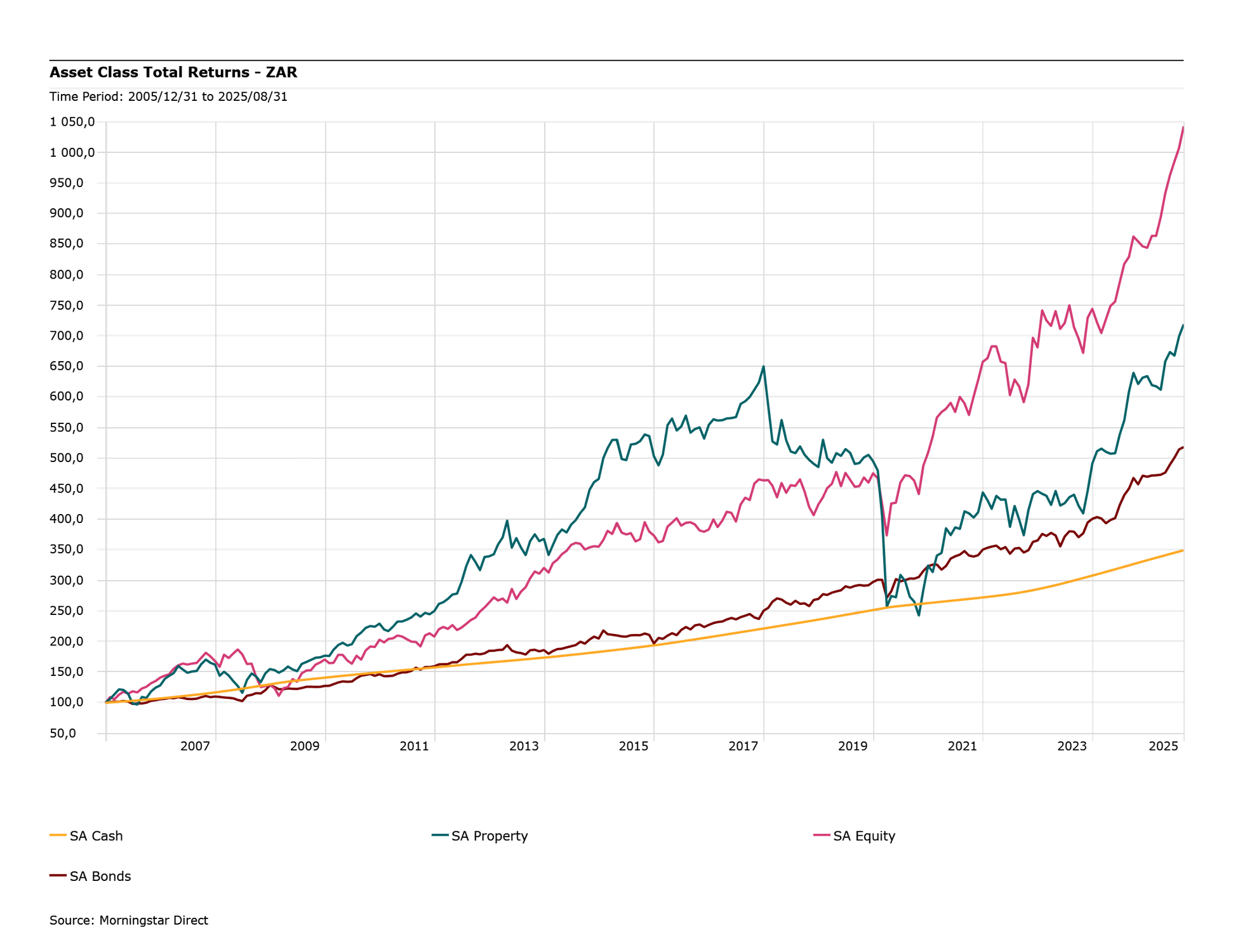

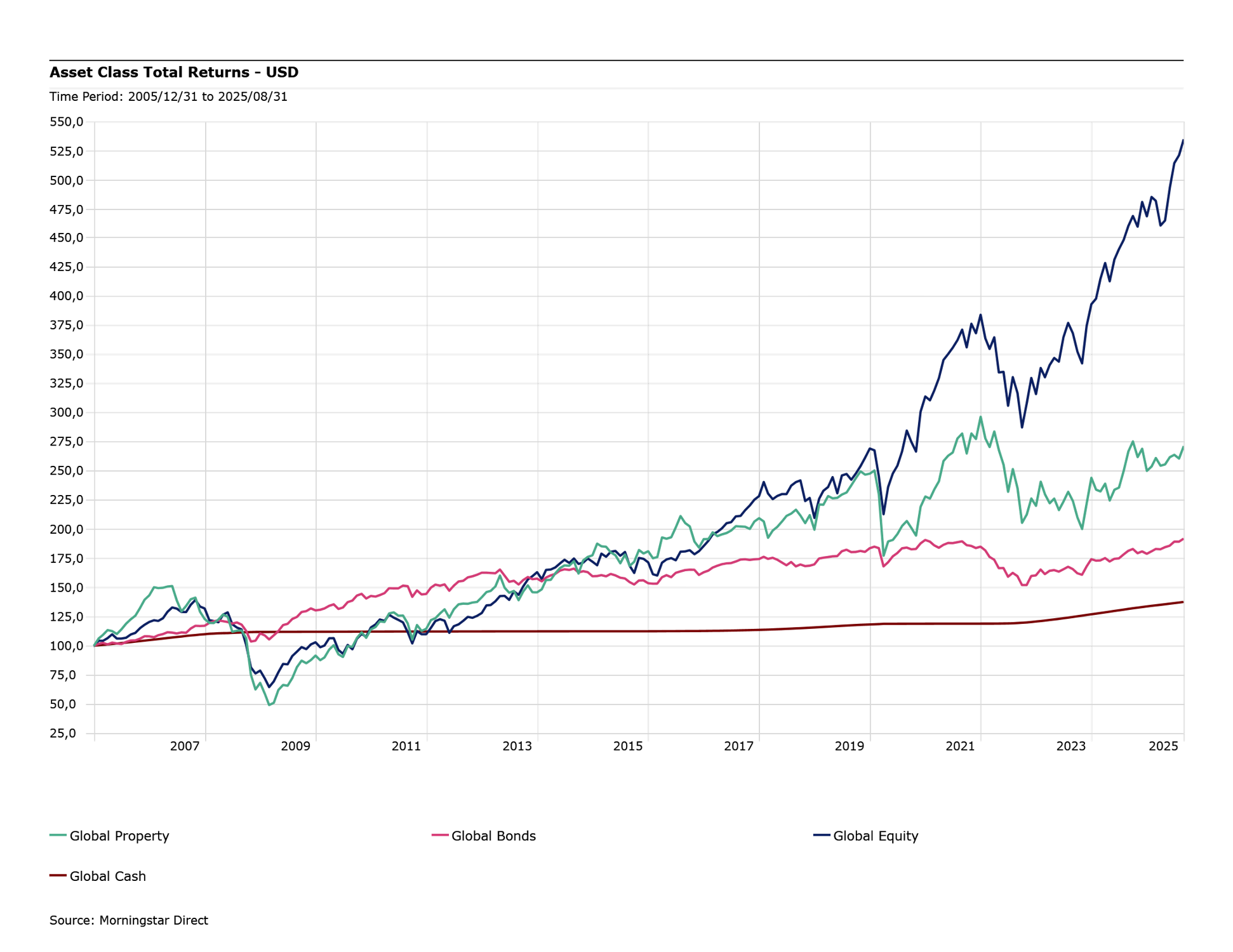

The relationship between risk and return is foundational to investment theory. Assets with more predictable future cash flows, like government bonds, tend to offer lower returns. Their stability comes at the cost of limited upside. Equities, on the other hand, are exposed to a wide range of unstable factors—economic shifts, competitive pressures, and changing consumer behaviour. This uncertainty translates into volatility, which is uncomfortable, but also necessary. Without it, there would be no incentive to invest beyond the risk-free rate.

Despite this, our natural aversion to uncertainty often leads us to make decisions that work against our long-term interests. We crave stability, and when markets fluctuate, we react emotionally—selling in downturns, chasing performance in rallies, or avoiding risk altogether. But avoiding risk entirely means accepting returns that may fall short of what we need to achieve our financial goals.

The answer is not to eliminate risk, but to take the right amount of it. Most investors tend to be cautious, sometimes to their own detriment, while a smaller group leans too far the other way, seeking risk for its own sake in pursuit of outsized returns. But this approach rarely pays off either. The higher the risk, the more dramatic the swings, and the harder it becomes to stay invested through market turbulence. Bigger drops demand stronger recoveries, and confidence can quickly erode. The most effective way to invest is not by aiming for the highest possible return, but by taking just enough risk to reach your destination.

What’s more concerning is when this imbalance in risk isn’t driven by the investor, but by the fund manager. There are cases where portfolios are constructed with far more risk than is necessary to meet the investor’s intended outcomes. This isn’t just inefficient, it reflects a deeper misalignment between the investment solution and the investor’s needs. The real value lies in partnering with an investment manager who understands how much risk is enough, and who works alongside the adviser to shape investment objectives and manage portfolios accordingly. When this partnership is strong, the strategy becomes purposeful; not a pursuit of performance for its own sake, but a considered approach that matches the investor’s journey with the right amount of risk.

Uncertainty, then, should not be feared, it should be understood. It is the reason markets exist, the reason prices move, and the reason opportunities arise. Without it, there would be no chance to earn more than the return on cash. But it must be approached with care. Risk is not something to be chased, nor something to be avoided entirely. It is something to be measured, managed, and matched to the investor’s needs.

By reframing uncertainty as a source of possibility rather than a threat, we can help investors build more resilient portfolios, make better decisions, and stay the course through market cycles. Because in investing, as in life, rewards never come without a cost. That cost is paid in the currency of uncertainty. The key is not to avoid it, nor to overspend it, but to use it wisely, and allowing time to do the heavy lifting. When wielded with care and patience, uncertainty becomes the very force that delivers meaningful rewards.