Market concentration is high today, but it’s not unprecedented. In 1965, the S&P 500 was also concentrated in a few dominant companies. Many of those firms later declined or disappeared, yet the index continued growing as new leaders replaced old ones. Market leadership rotates roughly every decade, and market cap weighted indices adapt automatically. The greater risk to long-term wealth is not concentration itself, but oftentimes investors reactions to it. History shows that attempts to time these transitions often result in missed returns. Broad diversification and disciplined investing remain the most reliable way to capture compounding through cycles of change.

Key takeaways

• Market concentration rises and falls over time. The current levels are historically high, but not unprecedented.

• The index compounds because it replaces declining leaders with emerging ones. Forecasting is not required for adaptation.

• The greatest threat to long-term returns is behavioural. Interrupting compounding through reactive decisions is far more damaging than concentration itself.

Concentration feels dangerous. History says otherwise.

Current market concentration is high, with ten companies representing about 40% of the S&P 500. That level of concentration hasn’t been seen since 1965. It’s the kind of statistic that makes otherwise rational investors start eyeing the exit. When leadership narrows, it feels like something that needs to be acted on. It sounds like a warning sign. But we’ve been here before. In 1965, the market’s giants were AT&T, General Motors, DuPont, Standard Oil and Kodak. They were dominant. Essential. Untouchable. Three eventually went bankrupt and the rest shrank dramatically in influence and size. It would be reasonable to assume that this would drag down the broader S&P 500 Index. Yet the opposite happened. The index continued to rise as leadership changed and new winners took their place. The index leaders changed completely, yet the index kept compounding.

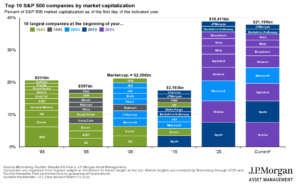

Chart 1: Top 10 weights as a proportion of the S&P500 & S&P500 Performance (RHS)

Leaders change. The index evolves

Every era produces companies that become giants. Strong performance builds confidence. Confidence turns into conviction. Conviction quietly becomes extrapolation and investors begin to assume that what has been true recently will remain true indefinitely. History suggests otherwise. Market leadership has rotated roughly every 10–15 years for more than six decades. Energy dominated in the 1970s. Japan represented nearly half of global equity value in 1989; today it is less than 5%. Technology surged in 2000, collapsed, and later returned in a different form. Financials led before 2008. Then something else took over.

Chart 2: Top S&P500 companies by market capitalisation as of first day of indicated year

Even the individual stories are sobering. Cisco briefly became the most valuable company in the world in 2000. It has still not reclaimed that valuation. Nokia once controlled 40% of global handset sales and later lost almost all of its peak value. These were strong businesses. The issue was not quality. It was the belief that leadership would persist without interruption. They were simply priced for permanence.

There is an older example that makes the point even more clearly. In 1900, the US stock market was heavily concentrated in railroads. Rail made up roughly 63% of US market value at the time. Today it represents less than 1%. That is not just a change in market leadership. It is a change in what the market even is. Yet rail as an industry still delivered strong long-run returns, even as its dominance faded and newer transport technologies emerged. The lesson is not that rail was “the winner”. The lesson is that market structure evolves, leadership rotates, and long-term compounding does not require investors to forecast which giants will still be giants decades from now.

What allows the market to move through these transitions is structural, not predictive. A cap-weighted index does not forecast the next winner. It gradually reduces exposure to shrinking companies and increases exposure to growing ones. As yesterday’s leaders fade, tomorrow’s leaders rise. The mechanism adapts even when investors struggle to. That is why the index compounds even when its giants do not.

The hidden cost is reaction

Periods of heavy concentration often coincide with elevated confidence. When a handful of companies drive most of the returns, it is easy to conclude that they are simply better, stronger, and more durable. Sometimes they are, but what tends to get overlooked is that the market already knows this. When expectations rise, valuations rise, and from that point, the future has to exceed already high assumptions.

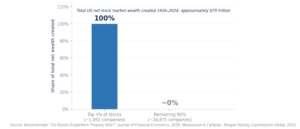

Research from Hendrik Bessembinder found that just 4% of US stocks created 100% of the net wealth generated by the US market over the long run. The remaining 96% collectively matched Treasury bills. If only a small minority of companiesdrive most long-term returns, and no one can reliably identify them in advance, then broad diversification stops being optional. It becomes essential.

Chart 3: Cumulative percent of wealth creation in US listed markets, all companies

The real problem arises when investors try to respond to concentration rather than understand it. Periods of narrow leadership tend to invite forecasts, strong opinions and portfolio shifts. Yet history shows that the biggest drag on long-term wealth has not been market concentration or even bear markets. It has been investor behaviour.

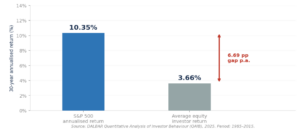

DALBAR’s long-running research captures this clearly. In 2024, the S&P 500 delivered a total return of approximately 25% (in USD)1, while the average equity investor earned materially less. Over multi-decade periods, the gap between market returns and investor returns has been even wider. The difference is not intelligence. It is the instinct to reduce exposure when uncertainty rises and increase exposure once confidence returns.

Chart 4: Investor returns vs market returns (DALBAR)

Stay invested. Let compounding work

The market does not reward investors for correctly naming today’s giants. It rewards those who remain invested when tomorrow’s giants emerge. Concentration comes and goes. Leaders rise and fall. The index continues adapting and compounding through each transition.

At PortfolioMetrix, investment management by design means building portfolios with genuine breadth, rebalancing systematically, and resisting the urge to react to short-term noise. We don’t bet on the survival of today’s giants. Our investing framework accepts that leadership will rotate. We do not try to predict which companies will dominate in 2040. We design portfolios that can evolve as markets do and we focus on the discipline required to stay invested while they do.

The giants will change again. They always have. The only question that matters is whether investors will still be compounding when they do. Compounding is a function of time, and any interruption, no matter how “rational” it feels is mathematically destructive.