Volatility is the price of simplicity

Why investing feels harder than it is and what actually matters

Investing is often described as complex, but the core principles are straightforward: stay invested, diversify, pay the appropriate fee, and allow time to do its work. What makes it feel difficult is not the rules, but the environment.

Volatility is not the same as risk and it is a natural and necessary feature of markets, not a flaw. Short-term volatility does not determine long-term outcomes. The decisions made in responses to volatility determine the outcomes and the challenge is that volatility creates pressure to act, which can interrupt compounding.

A well-structured portfolio is not designed to avoid uncertainty altogether, but to absorb it in a way that reduces the likelihood of reactive decisions. For many investors, the key to better outcomes is not more insight, but greater consistency in applying a sound process.

Key takeaways

- Volatility is not the same as risk; short-term price movements do not necessarily translate into permanent loss.

- The principles of investing are simple, but the experience of following them is often difficult.

- Behavioural responses to volatility are a major driver of long-term outcomes. The greatest threat to long-term wealth is not market movement. It is investor behaviour during it.

- Well-designed portfolios are behavioural infrastructure. It aims to manage investor behaviour as much as market risk.

- The challenge is not knowing what to do, it is doing it consistently when conditions feel uncertain.

The rules are simple. Following them is not.

Long-term investing rests on a small number of principles. Stay invested. Diversify. Focus on repeatable sources of return rather than binary predictions. Pay the appropriate fee. Allow compounding to work. Avoid large, irreversible mistakes. These ideas are not complex and they are not new. They are widely understood and largely agreed upon. Yet following them consistently is a different matter entirely.

The difficulty is environmental, not analytical. Investors operate in a world of constant information: headlines, forecasts, geopolitical events, and performance comparisons. Each development invites interpretation and, often, action. The result is a structural tension: simple rules applied in a complex and emotionally charged world.

“Don’t just do something, stand there.”

— Charlie Munger

There is an additional layer. As markets have become more efficient and investors collectively more sophisticated, the outcomes of the average active manager have become harder to distinguish from chance. In a world where luck and skill are difficult to separate in the short term, the instinct to respond to every new signal is not a strength, it is a vulnerability. This is where developing a robust portfolio construction process allows space to provide your investments time to work while looking through the noise.

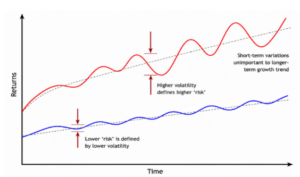

Volatility is the price, not the problem

When markets move sharply, investors feel something is wrong. A market decline is immediate and tangible, while the long-term outcome remains abstract. That gap between what is felt now and what will matter later creates a powerful instinct to act: reduce exposure, change fund managers, wait for clarity, or seek reassurance. Investors, however, look ahead to what is expected and once there is calmness in the markets the opportunity would likely already be behind you. This volatility is a normal feature of markets that generally rise.

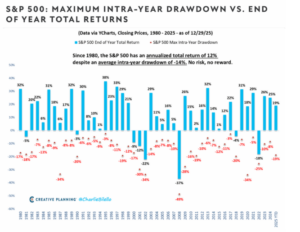

Source: Creative Planning. Past performance is not a reliable indictor of future performance

Short-term price movements reflect changing expectations and shifting sentiment. They do not, on their own, determine long-term outcomes. The volatility investors find so uncomfortable is structurally connected to the returns they are seeking. If outcomes were smooth and certain, there would be no reward for bearing uncertainty and you would receive the same returns as government bonds from the stock market or other assets. The discomfort is not a flaw in the system, but rather the fee that the system charges for participation and the pathway to the returns your goals may need.

“Risk is the possibility of permanent loss. Volatility is the presence of temporary fluctuation.”

— Howard Marks, Oaktree Capital

The question, then, is not how to avoid volatility. It is how to ensure that volatility does not provoke a decision that is difficult to undo.

The real damage is behavioural

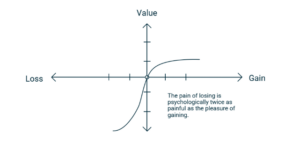

Periods of market stress rarely cause permanent harm on their own. What causes lasting damage is the response. Psychologists call it Loss Aversion: losses feel meaningfully larger than gains of the same size. The asymmetry makes investors more sensitive to declines than to recoveries, and more likely to act in ways that prioritise short-term comfort over long-term outcomes. The portfolio has not changed. The investor’s relationship with it has.

Source: PortfolioMetrix. For illustrative purposes only and does not constitute investment advice.

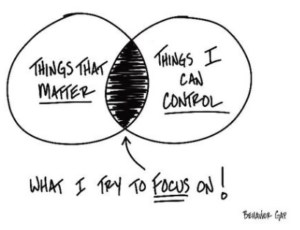

Michael Mauboussin, whose work on decision-making under uncertainty is particularly relevant here, identifies a compounding problem. In the short term, outcomes are heavily influenced by factors beyond an investor’s control. Yet short-term outcomes are what investors use to judge their decisions. The feedback loop this creates encourages exactly the wrong behaviour: reactive adjustments in environments where uncertainty is highest and information is least reliable.Carl Richards, author of The Behaviour Gap, frames the practical response clearly. What investors can control is not the market. It is the age at which they plan to retire, how much they save each month, and the risk level their asset allocation reflects. Acting as though the market is within that list of controllables is where the largest and most avoidable costs are generated. The cost is not theoretical.

Source: Behaviour Gap.

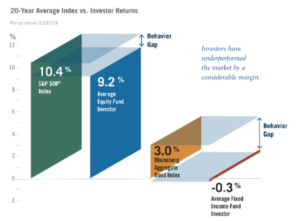

As a reminder, DALBAR’s annual research consistently shows a material gap between market returns and the returns earned by average investors. The difference is not intelligence. It is the habit of reducing exposure when uncertainty rises and increasing it once confidence returns. By then, the recovery has already happened.

A portfolio built for the real challenge.

Eliminating volatility is not the goal. Doing so would require reducing exposure to the assets that could generate long-term growth. The goal is to hold a portfolio where the level of volatility is within the range an investor can sustain without reacting. Portfolio construction is more than an exercise in asset allocation. A well-designed portfolio is built to manage investor behaviour as much as market risk.

At PortfolioMetrix, investment management by design means building portfolios with the structure to absorb volatility and the discipline to maintain it. We do not try to remove uncertainty from the investment experience. We try to ensure it does not drive the decisions that matter most.

Volatility is not the obstacle to long-term investing. In most cases, it is the condition that makes long-term investing worthwhile. The edge available to every investor is not a better forecast. It is a process that can be sustained when conditions make everything feel difficult.

The rules have not changed. The environment always will. Focus on the parts of the financial planning process you can control.