Why chasing unicorns can cost you returns

SpaceX could be one of the biggest public share offerings in history, potentially valued at close to $2 trillion – placing it as one of the world’s largest companies. Yet because only a small slice may be available to investors, its weight in a global equity benchmark will be much smaller. For long-term investors, the lesson is clear: don’t chase one rocket-fuelled unicorn on day one when broad diversification gives you exposure to hundreds of potential winners.

Key takeaways

- Unicorn IPOs are back in focus. Several major private companies may list soon, with SpaceX potentially the biggest of them all, possibly reaching a value of $2 trillion.

- Big valuation does not mean big portfolio weight. Even at a huge headline valuation, SpaceX may initially be a small holding in global indices because only a limited number of shares may be available to buy.

- Index exposure happens gradually. Passive investors are likely to gain exposure over time as new listings are added to indices, rather than all at once on day one.

- IPO excitement can be risky. New listings often come with limited trading history, low free float and high volatility, and many IPOs have underperformed after the initial hype.

- Diversification remains the sensible approach. Staying broadly invested allows portfolios to capture successful new companies over time, while avoiding the risks of betting too heavily on one stock at launch.

The ‘unicorn’ market

Back in the early 2010s the term ‘unicorn’ was given to privately-owned companies that were valued at over $1bn. In 2013, there were around 40 of these companies. Today, it is estimated that there are over 1,300. (Source: Value Add VC – Global Unicorn Companies Tracker)

A number of these ‘unicorns’ have successfully become public, including names which many of us know well, such as Airbnb and Uber. Several very large private unicorns have been speculated to be listing in the near future via an Initial Public Offering (IPO), including some well-known AI driven technology firms.

SpaceX is a big deal

The most high-profile of these is Elon Musk’s SpaceX. Based on information in their listing documentation, market commentators note that it is looking to raise money through an IPO later this month and with a possible valuation of somewhere between $1.75 and $2 trillion. This would make it one of the world’s largest publicly traded companies by size.

Since the turn of the century, the average amount raised by a company at IPO, has been around $250mn. (Source: SEC IPO Statistics 2000-2025) At a valuation of $2 trillion, SpaceX would be around 8,000 times larger than the average IPO.

But SpaceX’s founders and major backers are expected to retain a large portion of their shares. Elon Musk is also reportedly subject to a 1 year lock-up, meaning he cannot sell his shares during that period. As a result, the market currently expects that only 3-5% of the company’s shares would be made available to the public at the IPO, otherwise known as the ‘free float’.

The free float range for SpaceX is $60-100 billion of a total valuation of $2 trillion. Regardless, this would still be the largest IPO in the world, around 2 to 4 times the size of the previous largest IPO, Saudi Aramco, which raised $26 billion in 2019.

Why the free float matters

The free float is important because it tells investors how much of a company is available to buy. It is also a key driver of the company’s weights in most equity benchmarks.

On that basis, SpaceX’s initial weight in a global equity index like MSCI World could be around 0.1%, despite the headline valuation placing it near the very top of any size ranking.

The $2 trillion company and the 0.1% portfolio holding are the same company. The difference is how much of it is available for investors to own.

How the index inclusion process works

Large listings don’t arrive in global portfolios all at once. They come through in stages, and that sequencing is deliberate. Major index providers have specific criteria for including new companies, commonly linked to how long a stock has been trading for, free float size and financial criteria. In some instances, the inclusion can be fast-tracked, provided more stringent criteria are met – some, but not all, of which SpaceX meets.

Based on existing listing criteria it is possible that SpaceX may appear in a couple of major domestic indices after a week of trading, and then potentially in more indices, including global indices, within its first three weeks of trading. But it will take at least 12 months for it to be added to the most notable US index, the S&P 500 – again provided it meets all of the relevant criteria.

This staggered process gives the market some time to assess the price before new pools of passive capital, which are required to own the stock, enter the market.

How the investor base changes

As noted, passive investors will naturally gain exposure over time, but this is only after the stock has been trading and index inclusion begins. From day one active fund managers, pension funds, insurance companies and retail investors will be able to invest.

Pre-IPO investors are also important, and their impact depends on their lock-up periods. When founder and private investor lock-ups expire, those investors may sell some of their shares. This leads to more shares entering the market, the free float increases, and the index weight can shift materially. The portfolio weight of a new listing at day one and at month twelve can look very different. It will also mean capital is re-allocated away from other companies in the index.

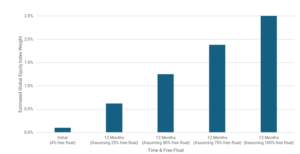

Chart 1: Illustrative global equity index weight of an IPO company (initial and after 12 months)

Illustrative example (not related to an expected outcome for SpaceX), based on internal modelling of a 4% initial free float, a company valuation of $2 trillion and a 0.1% global equity index weight, assuming no change to company values over that time

Some disciplined systematic investors are more cautious. They deliberately avoid new listings for the first year of trading. Their reasoning is that the conditions around a new listing, limited trading history and lock-up mechanics that can distort early price formation, are not well suited to long-term investment. The data supports this approach. Historical data suggests that many IPO cohorts have, on average, underperformed the broader market in the 12 months after listing – but the outcomes vary materially.

One company, or all of them

With that context, the real decision comes into focus. What should investors take into consideration when large companies IPO?

Buying SpaceX at listing means taking a concentrated position in one company, at a moment when excitement is high, free float is restricted, lock-ups have not expired, and index weight is minimal. Price discovery may be difficult and the share price is likely to be volatile for a while.

If the company performs exceptionally well, the upside can be significant. The downside falls entirely on that one position.

Staying broadly invested means that when SpaceX or another unicorn IPO reaches the scale and stability to enter major indices, a diversified portfolio picks it up. The return from any subsequent growth sits alongside hundreds of other companies. No single prediction is required and the risk is spread more widely.

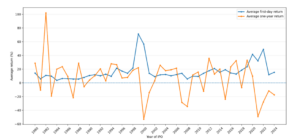

Research tracking US stock market listings over four decades shows a consistent pattern: the years with the biggest first-day gains were followed by some of the weakest returns over the next year. The 2021 class of new listings averaged a 32% gain on day one, then lost nearly half their value over the following year. (Source: Jay Ritter, University of Florida, Initial Public Offerings: Updated Statistics, 2025.)

Chart 2: Post-IPO returns by listing year

Source: Jay Ritter, University of Florida, Initial Public Offerings, Updated Statistics, 2025.

Note: Past performance is not a reliable indicator of future

The early surge rewards investors who were already in before trading started. The volatility that follows is what catches many others.

The gap that matters most

This is the important lesson for us all: the issue is not just what a new listing does, but what it encourages investors to do. There is a consistent difference between the return a market delivers and the return an investor receives.

Over long periods, broad markets compound. But investors do not always stay for the whole ride. When something feels urgent – a major listing, a company in the news, a window that seems like it might close – people can make moves they would not otherwise make. They shift from broad to specific, add risk they did not plan for, and when the volatility that almost always follows new listings arrives, they can end up selling at exactly the wrong time.

That gap is where most of the real cost sits.

Staying invested in a broad portfolio, rebalancing as markets move, and letting new companies earn their way in over time takes real discipline. Over long periods, that discipline is also where returns often come from.